Healthcare construction project starts fall by 13%

The healthcare construction industry continues to face challenges, with project starts falling by 13% in the three months to the end of April compared to the preceding quarter.

However, the figure is an increase of 26% on the same period last year, according to Glenigan’s Construction Review for April.

This light at the end of the tunnel provides some optimism that healthcare, along with the education and community and amenities sectors, may buck the trend being seen across all other verticals.

The report focuses on the three months to the end of March 2024, covering all major projects, worth more than £100m, and underlying projects, worth less than £100m, with all underlying figures seasonally adjusted.

And it reveals that:

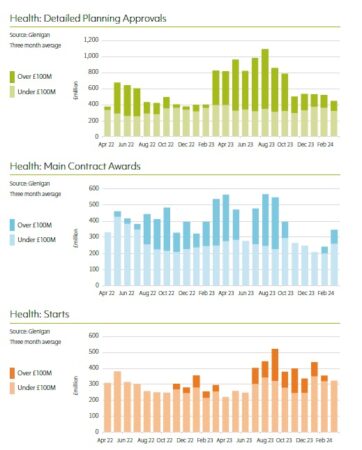

- Detailed planning approvals decreased against both last year and over the previous three months to April

- Main contract awards grew on the preceding quarter while project starts increased on a year ago, providing a boost to the development pipeline

- Adding up to £969m, underlying health work starting on site (less than £100m in value) during the three months to March fell 13% against the preceding three months on a seasonally-adjusted (SA) basis to stand 26% up against the previous year

- There were no major projects (£100m or more) starting on site, a decline against the previous quarter and last year

- Overall, health starts slipped back 4% against the previous quarter, but increased 9% on a year ago

- Totalling £1.03bn, health main contract awards were up 39% against the preceding three months, but 36% down against a year ago

- Major projects totalled £257m, up on the preceding three months where there were no major projects, but down 70% against the previous year

- Underlying contract awards experienced a mixed performance, decreasing 18% against the preceding three months (SA) to stand 4% up against the previous year

- Detailed planning approvals, totalling £1.3bn slipped back 17% against the preceding quarter and fell 46% on the previous year. Major project approvals, totalling £377m, decreased 38% against the previous quarter to stand 71% down against last year

- Underlying approvals, at £971m, experienced a 10% decrease (SA) compared with the preceding three months to stand 19% lower than a year ago

In terms of regions, the South West was the most-active area for health project starts during the first three months of this year, totalling £190m, having grown 37% against the previous year to account for 20% of total health project starts.

At £165m, the East of England accounted for a 17% share, with the value of projects in the region jumping by 157% compared with last year’s levels.

Health starts in London accounted for 14% and more than doubled compared with the previous year’s levels, totalling £139m, mainly thanks to the £80m South West London Tolworth Hospital development in Kingston upon Thames.

With a total value of £320m, the East of England was the most-active region for detailed planning approvals, having more than doubled on a year ago to account for 24% of the health sector.

Approvals in London also jumped nearly six times compared with the previous year to total £310m, a 23% share of health consents.

Somewhat predictably, hospitals accounted for 57% of health work starting on site during the three months to March, with the value having increased 42% against the previous year’s levels to total £553m.

And nursing home project starts, accounting for 18% of the sector, grew by 50% compared with the previous year to total £178m.

Accounting for 7% of health projects starting on site, dental, health, and veterinary centres increased 42% on a year ago to total £63m.

But, in contrast, day centres slipped back 59% to total just £1m, accounting for less than 1% of health project starts during the period.

The report also provides an insight into the leading contractors and clients within the sector, with the Department of Health remaining the top client, with 218 projects work £1.6bn, followed by Ellison Oxford, with one project worth £300m.

Canary Wharf and Laing O’Rourke topped the contractor tables, with projects worth £500m and £300m respectively.

Commenting on the figures, Glenigan’s economic director, Allan Wilen, said: “Sluggish performance in Q1 2024 is unsurprising as economic uncertainty continues to deter private sector investment.

“However, there are some small glimmers of hope to be found within some verticals, which experienced modest growth during the review period.

“Particularly work in education, health, and community and amenity indicates a small boost in the public sector pipeline.

“However, with a General Election approaching, any short-term improvement needs to be considered with a degree of cautious optimism.”