Construction time again!

Construction intelligence specialists are forecasting a return to growth within the healthcare building sector, with a recent fall in performance set to be followed by a 24% uptick by 2027.

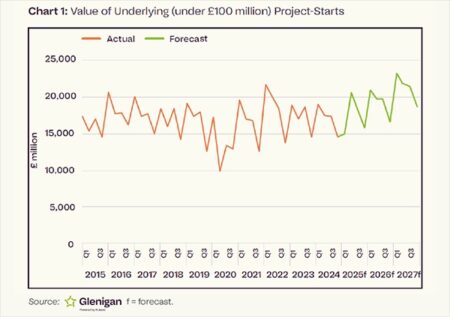

Glenigan | powered by Hubexo, one of the construction industry’s leading insight and intelligence experts, recently released its widely-anticipated UK Construction Industry Forecast 2025-2027. Predominantly focused on underlying starts (<£100m in value), it contains a comprehensive overview of the current state of the construction industry.

And the key takeaway from the Summer Forecast, which focuses on the three years 2025-2027, is that the sector will experience a much-needed resurgence in activity as the UK economy continues to improve and public funding for critical infrastructure increases following the recent Spending Review.

With growth predicted for 2025 (+3%), 2026 (+10%) and 2027 (+11%), these positive figures, spurred on by greater consumer and business confidence, will be welcomed industrywide, especially following a disappointingly-stagnant second half of 2024.

A reversal of fortunes

The reports states that, despite the promise of renewed growth, 2025 got off to a rocky start, likely experiencing a hangover from a disappointing 2024, which was rocked by socio-political turmoil at home and abroad.

However, as the Government found its feet over the spring, and more certainty started to return to the markets, the prospects of renewed growth appeared increasingly likely.

The main driver for this upturn has been a strengthening in domestic demand, particularly consumer spending amid heightened unease in global markets.

This is reflected in the recent uptick in underlying construction starts over the previous quarter, which is anticipated to remain stable following the various building and upgrading commitments made by the Chancellor in her recent speech.

Healthcare gradually recovers

Project starts in the health sector are expected to decline by 7% this year as the development pipeline contracted, disrupted by last year’s General Election and the new administration’s review of existing programmes, as it shapes its long-term strategy for the NHS.

The need to recalculate costs for major projects such as the New Hospital Programme has also led to a slowdown in the sector.

However, the additional capital funding announced by the Chancellor in the Budget, raising NHS capital spending to £13.6bn for 2025/26, is expected to boost sector activity in the second half of the year.

The promise of some refreshingly-strategic spending from the Government will certainly send a positive signal to contractors and sub-contractors nationwide, with spending earmarked for a number of big and small projects presenting plenty of opportunities

And this should partially offset the weak start and provide a solid foundation for growth later in the forecast period.

The Spending Review and the Government’s NHS 10-Year Plan have set out longer-term funding commitments from 2026/27 onwards.

And this increased capital investment is expected to support renewed growth in 2026 (+3%) and 2027 (+8%), according to the report.

Commenting on the forecast, Glenigan’s economic director, Allan Wilen, said: “It’s been a frustrating few years for the construction sector.

“Just as there seems to be light at the end of the tunnel, a new set of headwinds seems to buffer it, leading to prolonged stagnation.

“Yet recent events indicate we’re finally turning a corner.

“The promise of some refreshingly-strategic spending from the Government will certainly send a positive signal to contractors and sub-contractors nationwide, with spending earmarked for a number of big and small projects presenting plenty of opportunities.

“We should also not underestimate the mercurial nature of geopolitical events.

“While the US tariffs have caused turmoil across the world, the UK’s relatively-lighter treatment may help to renew private investors’ enthusiasm to put their money in our built environment.

“Of course, trade negotiations are ongoing and volatile, so construction businesses need to approach predicted growth with an element of caution.

“However, as it currently stands, the signs are positive and the industry can look forward to an extended period of increased activity.”

The publication of the Glenigan report comes just days after its May Construction Review, reflecting activity across all sectors in the three months to the end of April.

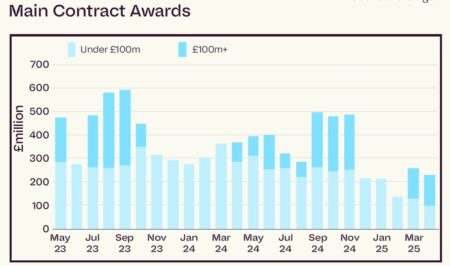

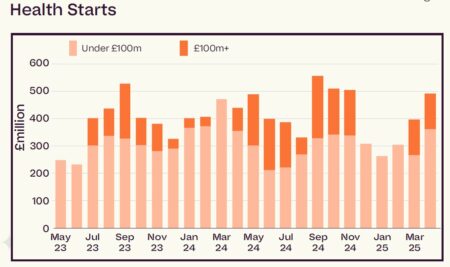

For the health sector, it shows that project starts rose by 87% compared to the preceding three months, while main contract awards increased by 7% over the same period.

However, detailed planning approvals – often an indication of the future pipeline – declined by 9%.

While the US tariffs have caused turmoil across the world, the UK’s relatively-lighter treatment may help to renew private investors’ enthusiasm to put their money in our built environment

The report states: “Health starts rebounded strongly during the three months to April, increasing by 87% to stand 12% higher than a year ago.

“The rise was accompanied by a strengthening in main contract awards.

“Less encouragingly, the development pipeline continued to contract, with detailed planning approvals 60% down on a year ago.

“Looking ahead, the outlook for the sector is cautiously optimistic, with a forecasted 1% growth in 2025 according to our most-recent forecast data.

“However, the marked decline in detailed planning approvals since the General Election highlights the rise of a potential gap in project starts as the NHS trusts’ development programme is still in limbo ahead of the 10-year plan for the health service in the summer.”

Project type

The health sector experienced a strong performance compared to the previous year, with three out of four segments experiencing increases.

- Hospitals accounted for the largest share (47%), having grown 11% year-on-year to total £689m

- Totalling £318m, the value of dental, health, and veterinary

centres/surgeries starting on site increased 214% on a year ago

to total £318m

- Nursing homes and hospices experienced a 22% decline against the previous year to total £153m

Regional activity

Northern Ireland at £501m was the most-active region for project starts, accounting for 34% of the total, with the region rising 980% against the previous year.

Growth in the area was boosted by the £389m Belfast Royal Victoria Hospital project.

The North East of England, at £48m, also experienced a strong period, more than quadrupling against the previous year (+330%) to

account for 3% of the total value.

The South West accounted for the largest share of planning approvals (25%), with an increase of 38% against the previous year; while London, at £49m, experienced the sharpest growth for planning approvals, rising 700% against the previous year to account for 9% of the total value.

The report also provides information on the leading contractors and clients for the three-month period. It shows that Laing O’Rourke (two projects worth £890m), Graham Construction (three projects worth £415m), and Morgan Sindall (13 projects valued at £197m) were the top three contractors, while the Department of Health, CPD, and the Central Laboratory of Research were the top three clients, with projects worth £1.9bn, £206m, and £85m respectively.